Practical Tips: Shareholder Agreements Explained for Minority Shareholders

Practical Tips: Shareholder Agreements Explained for Minority Shareholders

Picture this: You're the minority shareholder with 25-35% in a three-party joint venture.

Things start off fine, but soon the other two team up on the board. They push deals that benefit themselves more, block dividends even when cash is flowing, and limit the information you get. With no strong quorum or veto rights, your voice gets ignored and you're suddenly stuck with no real say or easy exit.

That's exactly why, as a minority shareholder, you need to negotiate solid protections upfront: board representation, unbreakable quorum rules, veto power on big decisions like dividends and related-party stuff, full information rights, and tag-along clauses. Without them, you risk getting outvoted, sidelined, and watching your investment suffer.

What is a Minority Shareholder?

A minority shareholder is any shareholder who does not control the company. In practice this usually means:

- Holding less than 50% of the voting shares (or less than the percentage needed to pass ordinary resolutions).

- Lacking de facto control even if shares are close to 50% (e.g., because other shareholders are aligned against them).

In a three-party equal-share setup (common in these agreements):

- If shares are split ~33%/33%/33%, every party is technically a minority (none has >50%).

- The minority-tailored agreement still protects each party by giving unanimous veto rights and board seats — this is very common when no single party wants to be dominated.

If shares are unequal (e.g., 50%/30%/20%), the 20% or 30% holder is the clear minority and needs the strongest contractual protections because they can be outvoted on ordinary matters.

What to Pay Attention to When Negotiating a Shareholder Agreement?

During negotiations, minority shareholders should focus on turning contractual rights into real power, because statutes and articles of association usually favour the majority. Prioritise the following:

- Board seat / observer rights: Even 10% should get a director (as in the minority version). Ask for an observer if a full seat is refused.

- Veto / reserved matters: Push for unanimity (or at least 80–90%) on key decisions (share capital changes, large capex, dividends, related-party deals, borrowing, exit, etc.). A 75% threshold + casting vote is dangerous for a minority.

- Quorum & meeting rules: Insist that every board/shareholder meeting requires at least one of your directors/representatives. Block any “reduced quorum on adjournment” clause.

- Information & inspection rights: Demand the stronger wording: you can request information “as you reasonably require”, plus visitation rights and monthly/quarterly detailed management accounts.

- Lock-up / transfer restrictions: Shorter initial lock-up (2 years max). Strong tag-along rights (you get to sell on the same terms if a majority sells). Pre-emption rights on new share issues.

- Anti-dilution & new capital: Require your consent (or pro-rata rights) before new shares are issued, especially if not all parties contribute equally.

- Dividend policy: Lock in a minimum payout percentage (or at least a clear policy) so profits are not simply reinvested for the benefit of the majority.

- Exit / deadlock mechanisms: Clear, fair valuation (independent expert, not majority-controlled), drag-along only with your consent or at a premium, and a workable buy-out on termination events.

- Non-compete & confidentiality: Make sure these are mutual and time-limited; don’t let the majority use them to restrict you unfairly after exit.

- Governing law & dispute resolution: Neutral venue (e.g., Hong Kong courts or arbitration in a business-friendly seat) and cost protections.

- General: Always require that this Agreement prevails over the Articles (both do this, but double-check). Add a “good faith / fiduciary-like” obligation if possible. Get tax, accounting, and legal advice on the specific rules in the jurisdiction you are in.

How to Draft Clauses Tailored for Minority Shareholders?

If the shareholder is not directly involved in drafting the shareholder agreement, there are several key aspects or clauses that the minority shareholder should check.

Board of Directors Clauses

- Minority shareholders should make sure that the agreement gives explicit board representation even to small holder

- For example, add “Any group of minority shareholders (aggregating not less than 10% of the voting rights), shall be entitled to appoint a director.”

Board Quorum

- The agreement should prevent the larger shareholders from meeting and deciding without the minority’s presence.

- For example, add clauses like “Must have at least one director from each of P1, P2, and P3 at every meeting. No reduced quorum on adjournment.”

Shareholder Meetings: Reserved Matters Approval

- Make sure that it requires unanimous vote of all Shareholders

- Unanimous vote means that there is true veto power for every party, regardless of majority or minority.

Financial Matters

- A pro-minority shareholder version forces cash returns and predictability.

- Review specific rules on auditors, and dividend policy.

Information and Inspection Rights

- There should be stronger and proactive access for the minority to monitor the company.

- Such information may include monthly management accounts, operating statistics, etc.

- For example, a party can demand information “in such form as a party reasonably requires.”

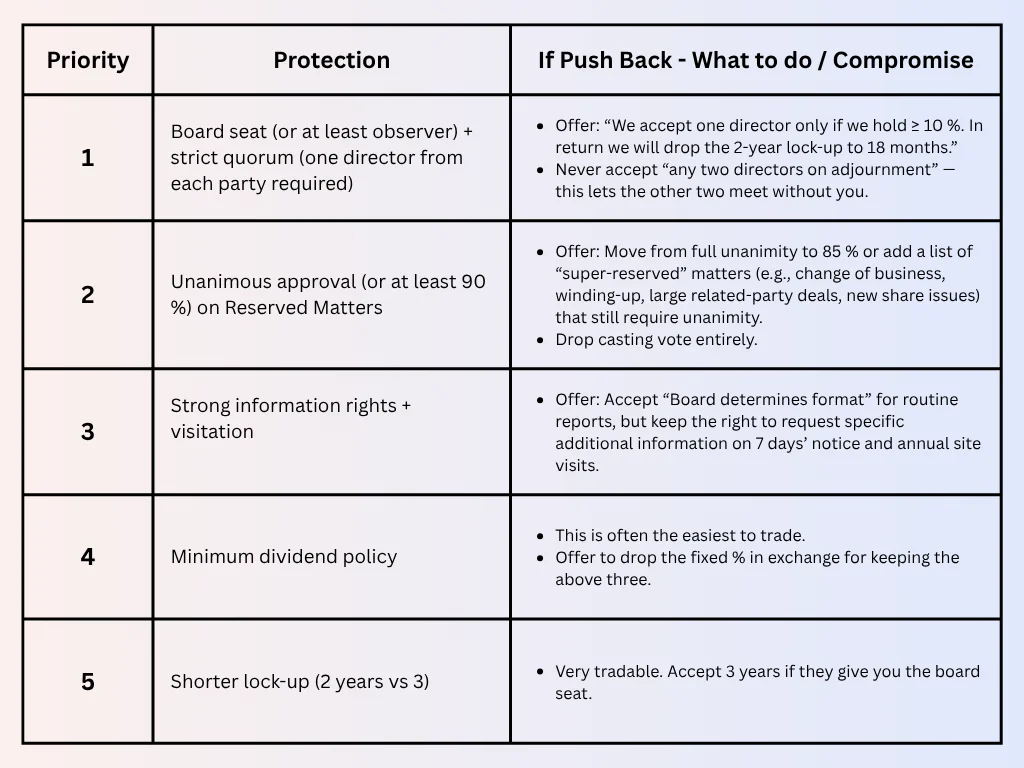

What if the Majority Shareholders Push Back?

If the other parties push back on stronger protections in the minority-tailored Shareholders Agreement, the minority shareholders’ goal is to trade concessions strategically while still securing non-negotiables: board representation, effective veto rights on reserved matters, and strong information/monitoring rights. These are the levers that actually give you influence once money is invested.

Before even sitting at the table, you should first know your leverage. Calculate exactly what percentage you will hold post-investment. If it is less than 30 to 35, you are objectively a minority. Use that to frame the discussion: “Because we are not equal in voting power, we need contractual balance to protect the joint venture.” In addition, be open to starting from a neutral position. Here is a table on what to prioritise most, ranking from the most important to the least important:

Even if you ultimately compromised in some areas, make sure the final agreement still contains:

- This Agreement prevails over the Articles

- Your nominated director can share information with you (explicit carve-out from confidentiality)

- Tag-along rights are fully preserved

- Expert valuation mechanism for any buy-out uses “Fair Price” without minority discount

2026 Template for Minority Shareholders (Important Clauses Only)

This is a template of Shareholder Agreement tailored for minority shareholders. The template assumes that there are three parties involved:

-----------------------------------------------------------------------

THIS SHAREHOLDERS AGREEMENT

Between

(1) [PARTY_1_NAME] whose principal place of business is at [PARTY_1_ADDRESS_SINGLE_LINE] (P1)

(2) [PARTY_2_NAME] whose principal place of business is at [PARTY_2_ADDRESS_SINGLE_LINE] (P2)

(3) [PARTY_3_NAME] whose principal place of business is at [PARTY_3_ADDRESS_SINGLE_LINE] (P3)

Whereas

(A) The parties have agreed to jointly invest in a company (the Company) in [TERRITORY] which it is intended will carry on business in the manner set out in this Agreement.

(B) The parties are entering into this Agreement to set out the terms governing their relationship as shareholders in the Company.

It is agreed as follows:

…

5. Board and Management

Supervision by the Board

5.1 The Board shall be responsible for the overall direction, supervision and management of the Company. The Board shall not, however, take any decision in relation to any of the Reserved Matters without the prior approval of the parties.

Board of Directors

5.2 The Board shall comprise of P1 Directors, P2 Directors and P3 Directors. Unless the parties agree otherwise, there shall be [P1_DIRECTORS] P1 Directors, [P2_DIRECTORS] P2 Directors and [P3_DIRECTORS] P3 Directors.

Quorum

5.3 The quorum for transacting business at any Board meeting (other than an adjourned meeting) shall have at least one of each P1, P2 and P3 Directors be present when the relevant business is transacted. If that quorum is not present within thirty (30) minutes from the time when the meeting should have begun or if during the meeting there is no longer a quorum, the meeting shall be adjourned for seven (7) Business Days and at that adjourned meeting any two (2) Directors (or their alternates) present shall be a quorum. A Director shall be regarded as present for the purposes of a quorum if represented by an alternate Director.

Notice and Agenda

5.4 At least 14 days written notice shall be given to each Board member of any Board meeting unless a quorum approve a shorter notice period. Any notice shall include an agenda identifying in reasonable detail the matters to be discussed at the meeting together with copies of any relevant papers to be discussed at the meeting. If any matter is not identified in reasonable detail, the Board shall not decide upon it, unless all Board members agree in writing.

6. Reserved matters

Use of powers

6.1 The parties shall use their respective powers to ensure, so far as they are legally able, that no action or decision relating to any of the matters specified in clause 6.2 (Reserved Matters) is taken (whether by the Board, the Company or any Subsidiary of the Company or any of the officers or managers within the Company Group) unless each of the parties has given its prior approval to proceed.

Reserved Matters

6.2 The Reserved Matters are:

(a) Memorandum and Articles

altering the Memorandum and/or Articles or other constitutional documents of the Company;

(b) changes in share capital

changing the authorised or issued share capital of the Company;

(c) change in nature of Business

materially changing the nature or scope of the Business (as described in clause 2.1) of the Company;

(d) Business Plan and Budgets

adopting the Business Plan or Budget;

(e) dividends

the Company declaring or paying any dividend or distribution;

(f) borrowings

the Company borrowing or raising money including entering into any finance lease, but excluding normal trade credit, which would result in the Company's aggregate borrowing exceeding [BORROWING];

(g) capital expenditure

the Company incurring any capital expenditure in respect of any item or project in excess of [CAPEX];

(h) acquisitions and disposals

the Company acquiring or disposing of (whether in a single transaction or series of transactions) any business (or any material part of any business) or of any shares in any company where the value of the acquisition or disposal exceeds [INVESTMENT];

(i) partnerships and joint ventures

the Company entering into (or terminating) any material partnership, joint venture, profit-sharing agreement, technology licence or collaboration;

…

Method of approval by Shareholders

6.3 The parties shall give their approval to any of the Reserved Matters (or to any variation of them) either in writing by the parties or by their authorised representatives for this purpose or by representatives of the Shareholders at a general meeting of the Company.

Meetings of Shareholders

6.4 General meetings of Shareholders shall take place in accordance with the applicable provisions of the Articles on the basis that:

(a) the quorum shall be one (1) duly authorised representative of each of the parties;

(b) the notice of meeting shall set out an agenda identifying in reasonable detail the matters to be discussed (unless the Shareholders agree otherwise);

(c) the chairman of the meeting shall have a casting vote; and

(d) a decision to approve any of the Reserved Matters shall require a supermajority vote (75%) of all the Shareholders.

Any matters requiring a general meeting of or approval by the Shareholders under relevant corporate laws, but not covered by the Reserved Matters, shall be dealt with in accordance with the Memorandum and Articles.

Deadlock

6.5 If a deadlock arises because the parties fail to agree on any of the Reserved Matters or any other management matter requiring their decision, the matter shall be referred to the respective Chairmen / Chief Executives of the parties with a view to the matter being resolved as early as possible in the best interests of the Company. Each party shall endeavour to resolve any disagreement in the best interests of the Company.

…

8. Information and reporting

Inspection and information

8.1 Each party may examine the separate books, records and accounts to be kept by the Company. Each party shall be entitled to receive all information in such form as the Board determines to keep it properly informed about the business and affairs of the Company and generally to protect its interests as a Shareholder.

Accounts, Business Plan and Budgets

8.2 Without prejudice to the generality of clause 8.1, the Company shall supply the parties with copies of:

(a) audited accounts for the Company (complying with all relevant legal requirements);

(b) a Business Plan and itemised revenue and capital Budgets for each Financial Year and showing proposed trading and cash flow figures, manning levels and all material proposed acquisitions, disposals and other commitments for that Financial Year; and

(c) monthly/quarterly management accounts of the Company.

…

29. Settlement of disputes

Amicable Settlement

29.1 If any dispute, controversy or claim between the parties arises out of or in connection with this Agreement, they shall use all reasonable endeavours to resolve the matter amicably. If one party gives the other notice that a material dispute has arisen and the parties are unable to resolve the dispute within a period of thirty (30) days of service of the notice, then the dispute shall be referred to the respective Chairmen or Chief Executives of the parties. Neither party shall resort to dispute resolution below against the other under this Agreement until thirty (30) days after the referral. This shall not affect a party's right, where appropriate, to seek an immediate remedy for an injunction, specific performance or similar court order to enforce the obligations of the other party.

Governing Law

29.2 This Agreement is governed by and shall be construed in accordance with the laws of [TERRITORY] applicable therein.

Dispute Resolution

29.3 Each party irrevocably and unconditionally submits to the exclusive jurisdiction of the courts of [TERRITORY] (and any court of appeal) and waives any right to object to an action being brought in those courts, including on the basis of an inconvenient forum or those courts not having jurisdiction.

30. Counterparts

This Agreement may be executed in any number of counterparts and by the parties to it on separate counterparts, each of which shall be an original but all of which together shall constitute one and the same instrument.

31. No rights for Third Parties

A person who is not a party to this Agreement shall have no right under any laws to enforce any of its terms.

As witness this Agreement has been signed by the duly authorised representatives of the parties the day and year above written.

Signed for and on behalf of [PARTY_1_NAME]

Signature: ______________________________

Name: ______________________________

Title: ______________________________

Date: ______________________________

Signed for and on behalf of [PARTY_2_NAME]

Signature: ______________________________

Name: ______________________________

Title: ______________________________

Date: ______________________________

Signed for and on behalf of [PARTY_3_NAME]

Signature: ______________________________

Name: ______________________________

Title: ______________________________

Date: ______________________________

-----------------------------------------------------------------------

For a full document, please visit Doclegal.ai. Doclegal.ai offers lawyer-reviewed shareholder agreements tailored for minority shareholders. You will be drafting the ideal agreement based on our template and our AI assistant. Starting from $10 today.